[By: Ernest P. Liang, 2015]

How We Erred On Stewardship

Much of the confusion regarding stewardship within the Christian community suffers from what may be called a misguided role reversal. A steward, in the modern parlance, is an agent who is engaged by the principal (master, owner) to look after his/her affairs. The idea is for the agent to seek the best interest of the principal in return for the trust, and reward, of the engagement. In a role reversal, the agent usurps the identity of the principal and acts to best his own interest, taking a ride on the contractual relationship wherein the owner becomes an impassive yet reliable provider of resources which the agent misconceives to be rightfully his own.

Believers acting on this misconception take seriously economic gains which they obtain by the sweat of their brow. They make financial decisions based on parameters that prioritize choices according to personal or familial desires while taking for granted the predictability of circumstances and the presumed boundless benevolence of the now owner-turned- agent Creator. To recast stewardship of financial matters in a proper framework requires resetting the parameters from a biblical perspective, righting the proper roles of agent vs. principal. This essay attempts to do that in the context of the decisions that define our everyday lives—how we spend, when we borrow, and what we must save.

To Buy Or Not To Buy—the Stewardship Of Consumption

“The world’s largest economy grew faster in the third quarter than first estimated, capping its strongest six months in a decade, as consumers went shopping…” flashed the headline from The Bloomberg News.1 For the U.S. economy, it is hard to overemphasize the importance of consumer spending which accounts for fully 70 percent of the national output. For the uninitiated and the pundit alike, consumption expenditure is good recipe for arresting economic stagnation, if not a sure prescription for sustainable economic growth (and by implication, the standard of living).

While politicians and economists debate (and they have for a long time) about the role of demand (as in consumption) in lifting economic welfare, the conscientious Christ follower often struggles with the exact boundaries of indulgence and contentment when stewarding over consumption. Just as the author of Ecclesiastes declares “So I commended pleasure, for there is nothing good for a man under the sun except to eat and to drink and to be merry, and this will stand by him in his toils throughout the days of his life which God has given him under the sun” (Eccl. 8:15 NASB), the Apostle Paul would fondly remind us that “But godliness is a means of great gain when accompanied by contentment. For we have brought nothing into the world, so we cannot take anything out of it either. If we have food and covering, with these we shall be content” (1 Tim. 6:6-8).

A proper exegesis of these passages, however, presents principles that are in perfect harmony. Recognizing God as the ultimate source of our happiness, the celebration of life in response to His provision and goodness duly brings forth enjoyment out of a gratitude to God’s loving kindness. A self-gratifying pursuit of material possessions and wonton pleasures is therefore a scorn to God’s promise of joy from a life of divine priority and valuable commitments. For when we define significance in terms of luxury and abundance, we would have lost sight of His kingdom and His righteousness, from which all these other things, Lord willing, are to follow (Matthews 6:33).

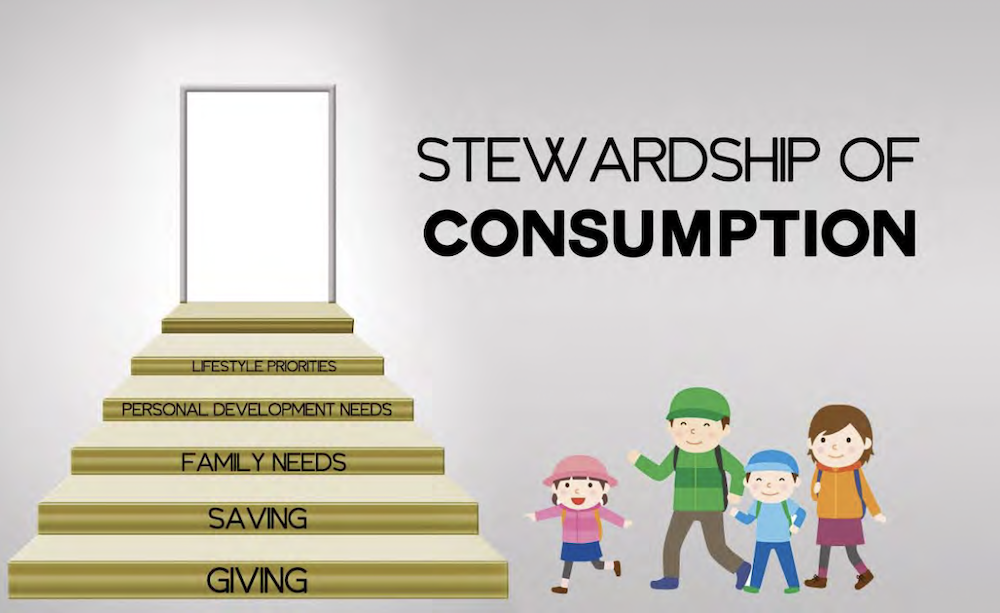

The stewardship of consumption is therefore best discussed in the context of biblical priorities. These priorities establish a framework within which a spending plan, or budget, may be constructed according to individual circumstances. In a world awash in affluence (by historical standards and undoubtedly in America), much confusion arises in the discussion of needs and wants, necessities and luxuries, relaxation and indulgence, etc. The framework presented below abstracts from these discussions by offering a guideline for priorities in Godly living. Starting with every dollar of disposable income, set aside portions that would meet these requirements (in the order presented). What is left for discretion beyond this list is, however, no less a testimony to one’s faith and maturity in a purpose-driven life.

- Giving— There is much written about giving in the Scriptures and in popular literature on Christian living. As Jim Elliott says, “He is no fool who gives what he can- not keep to gain what he cannot lose.” Giving is simply rendering to God what belongs to Him as testimony to our faithful stewardship of the resources entrusted to us. In setting priority for giving, two things stand out. First, sacrificial giving is pleasing to God, as evidenced by Jesus’ assessment of the widow’s act of sacrifice (Mark 12:41-44). Second, giving is a means by which the materially blessed share in kind God’s love and mercy to the less fortunate (thereby transforming corruptible earthly treasures into incorruptible heavenly treasures for themselves) (Matthew 19:21, Luke 16:7-9). As we contemplate giving, set a goal beyond what we ordinarily consider comfortable and cheerfully add para-church organizations serving the poor and needy to the recipient list. A faithful steward is held accountable for steering the entrusted resources to serve the master’s best interests, and giving is but the proper administration of this duty.

- Saving— From an economic standpoint even the consumption advocates would have to admit that supply must precede demand, that in order to spend we must first earn income by being gainfully employed. Savings, in the long run, constitute the source of funding for investment in business enterprises which offer the employment opportunities. At the personal level, savings meet the needs of contingencies and free us from societal/familial dependency after retirement. But perhaps the most important role of saving in the context of consumption is it enforces disciplined living. It is prudent to save a minimum of a quarter of the family’s annual income just to meet retirement needs.2 More should be set aside to provide for planned expenditures such as children’s college education and home or auto purchases. Something extra can be added to the pool to act as restraints on self-indulging non-necessities and impulsive purchases. More guidelines about savings are discussed later in this essay.

- Family Needs— The family (encompassing immediate and extended relatives) is the center of the covenant activity of God as portrayed in the Bible. Paul is quite un- equivocal in inserting the family into our financial priority when he writes, “But if anyone does not provide for his own, and especially for those of his household, he has denied the faith and is worse than an unbeliever” (1 Tim. 5:8). There is therefore no excuse for us to ignore the basic needs and comfort of our immediate, and perhaps even extended, family when we set spending priorities. We also need to recognize that as stewards of the family God has entrusted to us, we please the master by ensuring our family’s physical and spiritual well-being as well as by enabling the development of each member’s God-given potential. Faith-enriching education and other development activities such as Christian camps and mission trips would fall into this category.

- Personal development needs— Being a disciple literally means being a “learner.” As wise stewards of the talents, gifts, and time God has given to us, we need to be studious life-learners so that we become the best worker that can be and the shrewdest manager of God’s resources. Investing in learning through self-improvement and education (what economists called “human capital”), with a view to adding new skills (work related as well as social, emotional and thinking) and useful knowledge, is perhaps the smartest deployment of available financial resources. After all, the “good and faithful servants” in Jesus’ Parable of the Talents (Matthew 25:14-30) did not multiply their “talents” by sitting on their hands!

- What is left— The Bible does not lay out the Christian walk by pounding on believers a load of “don’ts” except for what are clearly sinful desires and actions. As we expend God’s resources, ponder on the guidelines in 1 Corinthians 10:23-24: “All things are lawful, but not all things are profitable. All things are lawful, but not all things edify. Let no one seek his own good, but that of his neighbor.” If that lacks specificity for some, then Calvin’s more direct advice may help: “While the liberty of the Christian in external matters is not to be tied down to a strict rule, it is, however, subject to this law—

He must indulge as little as possible; on the other hand, it must be his constant aim not only to curb luxury, but to cut off all show of superfluous abundance, and carefully beware of converting a help into a hindrance.”3

Till Debt Do We Part—the Stewardship Of Borrowing

Graduating from college is meant to be an occasion to celebrate. Unfortunately for many graduates, it is also a somber reminder that it is time to pay back what they owe. According to the Wall Street Journal, the Class of 2014 was the most indebted class ever.4 Over 70% of these graduates left school with student loans averaging a crushing $33,000. Student loans remain the fastest growing category (up over 360% since 2003) of U.S. household debt. Total U.S. household debt, on the other hand, grew 61% between 2003 and 2013.5 According to one report, the average American is more than $225,000 in debt with many having less than $500 in savings.6

In a society in which a certain perceived standard of living is regarded as a right of citizenship, and where the incentive to borrow is cemented by historic low interest rates and the prospect (even if illusory) of continued economic prosperity, the decision to go into debt often escapes serious scrutiny before the borrower signs on. To many, the question is not whether, but how much, to borrow, taking on presumptions upon tomorrow which may or may not be realistic. The Christian may face the additional conundrum of whether indebtedness is biblical at all, but the fact that everybody (from individual believers to congregations) is doing it often dispels any remaining doubt.

It may be comforting for many Christians to know that the Scripture does not prohibit borrowing. It is clear from both Old and New Testament passages that the practice of lending/borrowing, even at interest (whether in currency or in kind), seems to be accepted business procedures (Deut. 23:19, 2 Kings 4:1-7, Matt. 25:27, Luke 16:7-9). But given the fact that the vast majority of debt in biblical times were incurred by the poor or needy to meet basic consumption needs, the proper context of loans in God’s word is more like an act of love. As a result there is clear advice regarding the pledge of security (Deut. 24:6, Prov. 6:1), the need for release (Deut. 15:1-6), the evil of usury (Lev. 25:37), and the risk of enslavement (Prov. 22:7).

In today’s modern economy our needs have grown much beyond basic day-to-day consumption. For example, by defer- ring consumption we can lend relatively safely for a positive rate of return and borrow (leverage) to invest in increased productivity, contributing to a higher standard of living for all. Savings to build a retirement nest egg and borrowing to earn an education illustrate the point. For the modern Christian facing a confusing array of needs and wants, what could be sensible instructions on borrowing based on the Scripture? The following guidelines (acronym “PASS”) which adhere to the general biblical principles of stewardship and a purpose driven life, may be proposed:

- Profitability (P)— A borrower’s ability to repay a loan with interest is undergirded by the accretive purpose of borrowed funds. The use of credit is to enhance, or leverage, the potential return of an investment. A loan purely for the purpose of current consumption, such as a vacation or a new entertainment system, does not leverage, but one that augments future productivity, such as a college education or a new stamping machine for a machine shop does. Because credit card usages are primarily for services and ongoing consumption needs, to incur cumulative credit card debts requiring recurrent interest payments is not advisable. In contrast, our primary residence and private transportation means could be viewed partly as capital investments as they do contribute to our ability to lead and grow a productive work-life. Home mortgages and auto loan for the family car can perhaps be justified to the extent that most people would find it difficult to acquire these assets with savings alone.

- Affordability (A)— The primary obligation of the borrower is to repay the debt in full. According to Scripture, it is wickedness when one fails to do so: “The wicked borrows and does not pay back, but the righteous is gracious and gives” (Ps. 37:21). A prudent calculation on affordability will make sure a baseline discretionary cash flow (after budgeted giving, savings, and necessary expenditures but before debt service) is sufficient to service the debt until its maturity. If affordability is marginal, but the debt serves a good purpose, then the borrower should make sure there are enough assets that can be sold to repay the debt if necessary. Prudence in this context is to ensure plentiful margins so that one does not fall into insolvency.

- Speculation’s Folly (S)— It is paramount to consider the ability to repay a loan in unconditional terms, without making presumptions upon an uncertain future. The Book of James speaks to the folly of speculating about the future and the wisdom of a purpose driven life: “… you do not know what your life will be like tomorrow. You are just a vapor that appears for a little while and then vanishes away. … you boast in your arrogance; all such boasting is evil. Therefore, to one who knows the right thing to do and does not do it, to him it is sin” (James 4:13-17). It is “arrogance” when people think they can somehow force square pegs into life’s round holes or trust in their ability to restack life’s circumstances to bring about favorable outcomes. If a loan requires picking up a second job or putting the spouse or a child to work, then it would be wise to first seek spiritual affirmation regarding whether the debt is consistent with God’s purpose for our life. The same can be said about one’s tendency to rely on the speculative future appreciation of assets to justify their acquisition with debt (example: flipping houses for profit during the 2008 financial crisis). We need to be reminded that a first principle of assuming debt, as laid out in the Pentateuch, is that such a transaction needs to be pleasing to both God and man. Despite the vast difference in economic circumstances between now and biblical times, the Godly wisdom about lending and borrowing never changes.

- Stewardship (S)— Stewardship is all about serving our master for the best of His interest. With respect to resources entrusted to us by our heavenly Father, Jesus’ Parable of the Talents (Matt. 25:14-30) is most revealing. The wicked servant was rebuked and punished for his laziness, for failing to earn a minimum, risk free rate of return in bank interest. The faithful servants were praised and rewarded for their willingness to invest prudently and make a return over and above the opportunity cost of money (the bank’s interest rate), which required discernment and some risk taking. How is this principle applied to the taking on of debt?

If we have discretionary resources that are generating a certain rate of return and a new investment opportunity arises, is it prudent to fund this new opportunity with debt instead of the existing resources? The simple answer is yes if the cost of borrowing is less than the rate of return earned on the existing investments. The more complete answer will depend on the riskiness of the new opportunity, the terms of the loan, and the predictability of the returns on the existing investments. What is reasonable to say is that it is not always true to the statement “never borrow if you can afford not to.” What is important is that we put God’s entrusted resources to profitable use with wisdom, and all the guidelines discussed in here, nicknamed “PASS”, should be considered in their totality and not in isolation. Only in that way can we be wise users of debt.

The Crisis Of Financial Insecurity—the Stewardship Of Savings

According to a recent study by the Employee Benefit Research Institute, one-third of all American workers have a measly $1,000 saved for their retirement years. It says that 43% of Boomers and “Generation Xers” are at risk of running out of money in retirement. Among the poorest 25%, EBRI estimates a stunning 83% are at risk. Even more alarming, even these bleak numbers are based on the most optimistic financial scenarios!7

This savings crisis happens against the backdrop of a stagnant average U.S. household income, which according to the U.S. Census Bureau, has barely grown in real terms since the late 1990s. In a culture where the lure of material comfort, pleasure, and status is tantalizing, it is little wonder that excessive consumption reigns as norm, resulting in historically low personal savings rates (of below 4%).

For Christians, it is clear the Scripture touts the virtue of savings. But it needs to be put into proper perspective. Since God is the rightful owner of all we have, our role is faithful steward and not hoarder of resources. Jesus’ teaching in Matthew 6:19 (“Do not store up for yourselves treasures on earth”) and the parable of the rich fool (Luke 12:15-21) make the point quite clear. To further the emphasis of trusting God in all circumstances, the Apostle Paul was quick to point out that “if we have food and covering, with these we shall be content” (1 Timothy 6:8). Likewise the writer of Hebrews reminds us:

“Keep your lives free from the love of money and be content with what you have, because God has said, never will I leave you; never will I forsake you” (Hebrews 13:5). What then, would be the objectives of savings given these Scriptural teachings on contentment and trusting in God?

- Savings induce disciplined living— The overflowing abundance in our society often overwhelms our senses of living within our means, even if we sincerely desire so. In Proverbs 21:20, (“There is precious treasure and oil in the dwelling of the wise, but a foolish man swallows it up”) the contrast between the wise and the fool is not so telling in what they ended up as in how they got there—the act of squandering or devouring the resources entrusted to our care by God sets apart the foolish from the wise. Planned saving forces us to live responsibly. It is simply an act of wisdom in a materialistic world.

- Savings minimize our reliance on debt— As a financial economist I recognize the productive purposes of lending and borrowing in the modern economy. Even in personal finance, borrowing to acquire big-ticket assets (such as a home) that grow in value makes good economic sense as long as the debt service fits into a well thought-out budget with planned savings. Savings, however, keeps us out of unwarranted indebtedness which, after all, is enslaving and markedly inflates the total cost of a good or service (a form of “swallowing up” according to Proverbs 21:20). Saving is making provision for tomorrow, while debt is presumption upon tomorrow. Habitual indebtedness is both poor testimony and un- faithful stewardship. This is why Paul admonishes thus “let no debt remain outstanding…” (Romans 13:8) and Proverbs 22:7 cautions, “The rich rules over the poor, and the borrower becomes the lender’s slave.”

- Savings answer to times of need— While life’s uncertainties are enough reason for prudent saving practices, what Joseph did in Genesis 41 speaks to the necessity of careful planning for needs foreseen. Chief among these anticipated needs is the maintenance of a decent quality of life after we retire, when our income abilities diminish and our health inevitably deteriorates. Moreover, our withdrawal from the active workforce does not obviate our continued obligation to provide financially for our loved ones, which include not only our spouses but perhaps also our elderly parents and grown children should circumstances demand it. Paul is unequivocal in stressing the importance of a family safety net when he writes: “But if anyone does not provide for his own, and especially for those of his household, he has denied the faith and is worse than an unbeliever” (1 Tim. 5:8).

- Savings offer the freedom for ministry— Throughout Scripture the teaching on wealth has been remarkably consistent—it is a blessing in God’s sovereignty towards those who are faithful and obedient, and it is a curse towards those who are “not rich toward God” (Luke 12:21). Therein lies the difference between saving and hoarding. Hoarding is wealth building for self-glorification, and saving is wealth building for fulfilling our witness to God’s loving kindness. Not only is saving good stewardship because we can give to God’s work (cf. 1 Corinthians 16:2), but it is also our responsible answer to the Lord’s command about “not to worry about our lives” (Luke 12:22)—so that we can devote ourselves “worry free” to worthwhile ministries. While retirement is almost obligatory in modern secular work, it is not a known practice in the Scriptures. As we labor for the Kingdom in our advanced years, adequate savings would provide the freedom and means we need to be generous towards God.

- Savings bring a legacy of stewardship— Bequeathing an inheritance of material possessions is a virtue just as much as good character if it is built with integrity, discipline, and an eye towards nourishing our grandchildren to become good citizens of the Kingdom. Proverbs 13:22 appears to affirm this with the proclamation: “A good man leaves an inheritance to his children’s children, and the wealth of the sinner is stored up for the righteous.” The wisdom of this, however, is balanced on the understanding that the beneficiaries must be ready, wise stewards themselves. Proverbs 20:21 thus cautions: “An inheritance gained hurriedly at the beginning will not be blessed in the end.” Andrew Carnegie was correct when he suggested that “the almighty dollar bequeathed to a child is an almighty curse.” Even for the trained child, it would perhaps be prudent to leave enough to help fund worthwhile education and head starts on business. Any- thing in excess could easily be turned into a curse.

Larry Burkett said, “You can tell more about the spiritual lives of a couple by looking at their check book than by any- thing else.”8 Savings, planned with the express intent of giving for the glory of God, is a practice that enriches spiritual lives, a discipline of faithful stewardship. It is perhaps no coincidence, therefore, that both savings and salvation stem from the same root word.

About The Author

ERNEST P. LIANG is Director of the Center for Christianity in Business and Associate Professor of Finance at Houston Christian University. Prior to his academic career, he spent 25 years as a finance executive in firms ranging from technology start-ups to Fortune 500 companies, as chief economist of an economic consultancy, and as a principal of an advisory for middle market transactions and executive recruitment. Trained as an economist but practiced as a finance professional, he holds a Ph.D. and an MBA from the University of Chicago.

ERNEST P. LIANG is Director of the Center for Christianity in Business and Associate Professor of Finance at Houston Christian University. Prior to his academic career, he spent 25 years as a finance executive in firms ranging from technology start-ups to Fortune 500 companies, as chief economist of an economic consultancy, and as a principal of an advisory for middle market transactions and executive recruitment. Trained as an economist but practiced as a finance professional, he holds a Ph.D. and an MBA from the University of Chicago.

Notes

* Portions of this essay were previously published in blogs appearing in The Kingdom Economy (hc.edu/TKE), an online resource site for business professionals sponsored by the Center for Christianity in Business at Houston Christian University.

1 Victoria Stilwell, ”Spending by Households, Companies Propels U.S. Economy,” Bloomberg News, Nov. 25, 2014. Accessed 2014, www. bloomberg.com/news.

2 This is a rough rule of thumb based on a saver aiming to retire in forty years with no loss from the current standard of living but leave a cashless estate. A low interest/inflation environment is also assumed. The required amount goes up considerably for an older worker and one who aims to build cash into the inheritance.

3 John Calvin, The Institutes of the Christian Religion [1537], tr. Henry Beveridge, Online Library of Liberty, Chapter 10, Sec. 4. Accessed 2015, http://oll.libertyfund.org/titles/calvin-the-institutes-of-the- christian-religion?q=curb+luxury#Calvin_0038_1726.

4 Phil Izzo, “Congratulations to Class 2014, Most Indebted Ever,” Wall Street Journal, May 16, 2014. Accessed 2014, http://www.wsj.com.

5 Neil Shah, “U.S. Household Debt Increases,” Wall Street Journal, May 13, 2014. Accessed 2014, http://www.wsj.com.

6“In Today’s Economy, Average American is ‘Drowning’ in More Than $225,000 of Debt,” www.gobankingrates.com, September 10, 2013.

7 Brett Arends, “Our Next Big Crisis will be a retirement crisis,” March 3, 2014. Accessed 2014, http://www.marketwatch.com. See also Mandi Woodruff, “One Third of Americans only Have 1,000 Saved for Retirement,” March 18, 2014. Accessed 2014, http://finance.yahoo. com/news.

8 Larry Burkett, The Complete Financial Guide for Young Couples (David C. Cook, 1960), p. 19.